The Texas Land Market Is Not One Market

Landowners and capital allocators treating Texas as a monolithic land market in 2026 are making a pricing error. The data does not support a single narrative. What is emerging is a bifurcated market — one tier for land that is positioned, entitled, and utility-ready; another for land that is raw, speculative, or misaligned with where builders are actually buying.

That gap is widening. Understanding which side of it your property sits on is the most important underwriting question of the year.

Where Builder Demand Is Actually Concentrating

Builder permit activity in January 2026 confirmed what acquisition teams already know: capital is concentrating in specific corridors, not spreading evenly across the state. Dallas led all Texas metros in overall permit volume, with an average new home construction value exceeding $383,000 per unit. Collin County is commanding executive-level product. Tarrant County reflects consistent production builder volume. Williamson County continues to attract sustained development interest in the Austin metro, driven by land availability, infrastructure expansion, and relative affordability compared to central Austin.

The outliers matter too. Austin starts are down 15 percent year-over-year — the sharpest pullback in Texas — driven by the same COVID-era overbuilding that inflated prices. But Austin's long-term constraint is structural: water limitations and entitlement bottlenecks cap supply. That makes well-positioned Austin-area land a rebound asset, not a distressed one. Builders who understand that are already watching the pipeline.

San Antonio builders are largely self-developing rather than purchasing lots from master-plan developers. That dynamic changes how land is priced and who the qualified buyer pool is for landowners in that market.

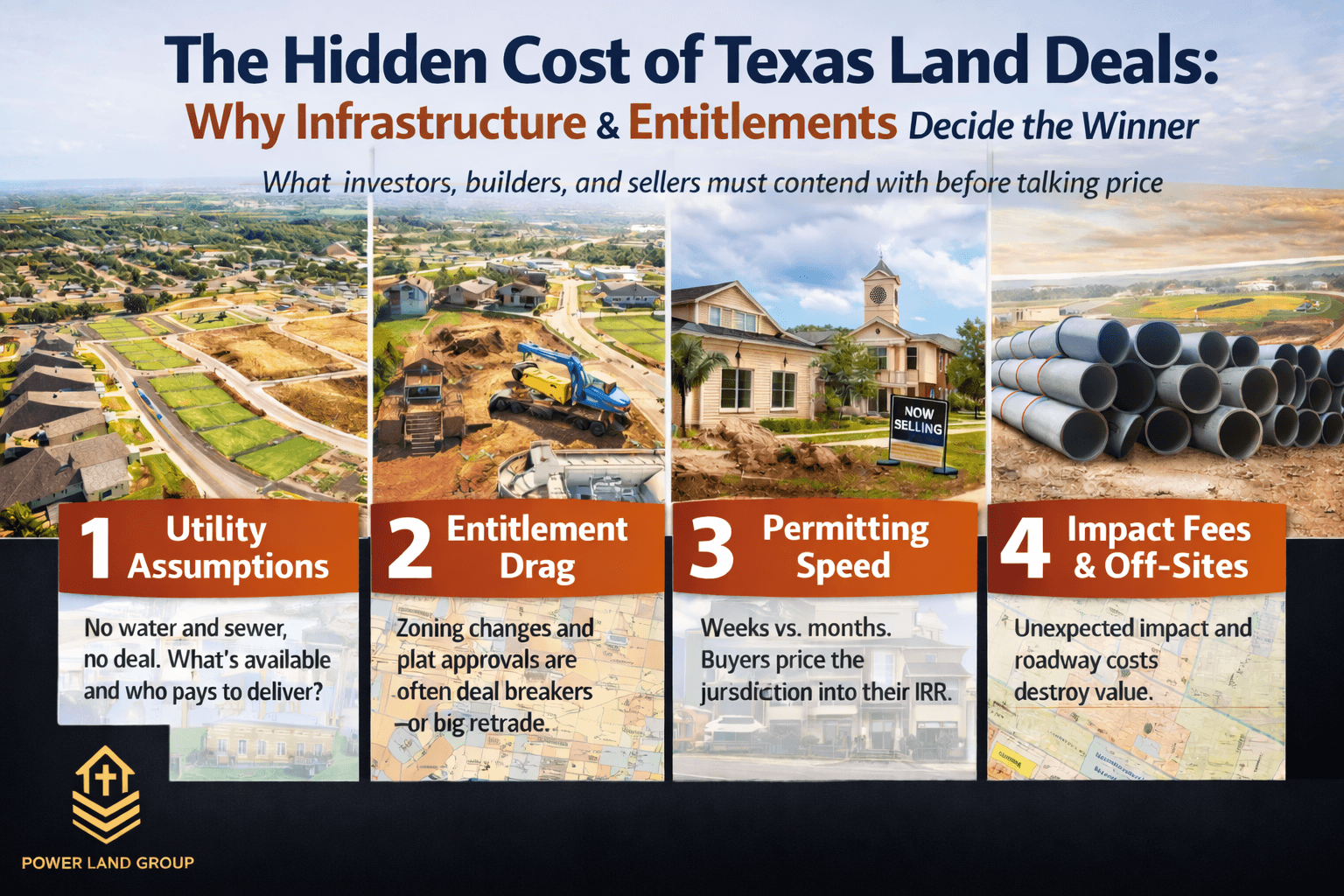

The Infrastructure Cost Problem Builders Are Pricing In

Utility and infrastructure costs are no longer a line item — they are a deal structure variable. Projects requiring significant utility or drainage work are adding 10 to 15 percent to overall construction cost per square foot. That cost lands directly on the land residual in a builder's pro forma.

In North Texas, the North Texas Municipal Water District is investing an estimated $1.7 billion in capital improvements in fiscal year 2026 alone, following nearly $1.2 billion deployed in 2025. Wholesale water rates for member cities are rising — up 7.5 percent year-over-year to $4.14 per 1,000 gallons in 2026, with further increases projected. These costs flow downstream to developers and ultimately compress what builders can pay for raw land without utility infrastructure in place.

This is the mechanism landowners most often miss. A builder does not price land in isolation. They price land net of all costs to get to a finished lot. When those costs rise, land prices compress — even if the end home price holds flat. Positioned land with utility access, road frontage, and entitlement clarity absorbs cost pressure. Raw land absorbs it fully.

What the Regional Price Data Actually Shows

Texas land price data for 2026 is not uniform, and averaging it obscures the real signal. The Austin–Waco–Hill Country region recorded a price increase of 3.4 percent year-over-year to a new high of $7,704 per acre, with sales volume rising 5.7 percent — the highest activity level in two and a half years. Northeast Texas saw prices appreciate 4.4 percent year-over-year to $9,313 per acre despite an 18.3 percent drop in sales volume. Price held because well-located supply remains constrained. The Panhandle–South Plains market trended sideways, with prices encountering resistance at elevated levels.

Development land near metro cores prices differently from rural acreage. Within 30 miles of downtown Austin, development land is commanding $100,000 to $500,000 per acre. Collin and Williamson counties are trading in the $9,000 to $12,000 per-acre range on average. The spread between well-positioned development parcels and raw land is not a premium — it is the cost of entitlement work and infrastructure investment already embedded in the price.

The statewide baseline forecast from Texas A&M's Real Estate Research Center projects nominal price per acre rising approximately 2 percent over the next four quarters through third-quarter 2026. That is a modest gain. It is not the tailwind that justifies holding a raw parcel indefinitely while carrying costs accumulate.

What Institutional Buyers Are Looking For Right Now

Institutional capital and private equity are allocating to real assets in 2026, with a specific focus on inflation protection and stable income. What separates actionable land acquisitions from passed deals comes down to four variables: utilities, entitlements, execution timeline, and realistic pricing. Builders are adjusting quickly — offering smaller homes on tighter lots to hit affordable price points, prioritizing standing inventory absorption, and being selective on new land acquisitions.

The builders and capital partners actively acquiring land in Q1 2026 are not chasing raw acreage. They are buying execution certainty. That means entitlements in hand or a clear path to them, utility capacity confirmed, and a land price that pencils against current home pricing — not 2022 comps. Landowners who present their property without that analysis are not competing for the same buyer pool.

In DFW, the market's employment base remains the strongest underwriting argument. Dallas alone added an estimated 40,000 to 50,000 jobs in the past year, and over 120 corporate relocations have landed in the metro over the last five years. Population demand is real. But builder selectivity is also real. They are moving to the suburbs and outer corridors — Prosper, Celina, Mansfield, Weatherford — where land pricing and infrastructure alignment still allows product to pencil at attainable price points.

The Decision Framework for Landowners in 2026

If you own raw or partially entitled land in a Texas metro corridor, the relevant questions are not what the market is doing in aggregate. They are:

- What is a builder's actual residual land value on your parcel today, net of infrastructure costs?

- Does your utility and entitlement position compress or protect that value?

- Is the exit market a local production builder, a regional operator, or an institutional land fund — and do you know which one is the active buyer for your specific product type?

- What does your carry cost look like over the next 18 to 24 months if the market continues its measured recovery pace rather than accelerating?

These are underwriting questions, not brokerage questions. The landowners who are transacting successfully in this market are not the ones with the highest asking prices. They are the ones who understand their property's execution story and can communicate it to a builder the way a developer would.

The Misread That Is Costing Owners

The most common mistake in the current Texas land market is conflating price resilience with liquidity. Prices have held in most corridors. That is accurate. But holding periods are extending, days on market are rising for unpositioned properties, and buyer pools are narrowing to operators who can execute — not investors who are simply land banking.

A well-located parcel with a credible path to entitled, utility-served lots will trade. A raw parcel with an aspirational price based on 2022 comparable sales will sit. In a market where builders are absorbing standing inventory and managing margin pressure through incentives, they are not overpaying for execution risk on the land side.

That dynamic makes a current, builder-driven land value opinion more valuable than a traditional appraisal. Appraisals look backward. Builders price forward.

PLG's Position

If you want a confidential Land Value Opinion or want to discuss positioning your property for institutional buyers, PLG evaluates land the way builders do — utilities, entitlements, execution timeline, and realistic pricing before we ever discuss terms. Submit your property details at powerlandgroup.com.