The Market Has Stabilized. Builder Discipline Has Not.

Texas is not in a land crisis. It is in a precision market. The post-pandemic surge is over. What remains is a state where population growth is structurally intact, builder demand is active, and institutional capital is circling — but every land transaction is being underwritten harder than it was 18 months ago.

Landowners who treat 2026 like 2022 will not transact. Those who understand how builders are evaluating sites right now will.

Here is what the data is telling us.

The Demand Signal Is Real — But It Is Market-Specific

Texas is still the center of American homebuilding. Single-family permits are projected to reach approximately 169,000 in 2026, reflecting roughly a 4 percent increase over 2025 trends, driven by stabilizing interest rates and steady underlying demand. That is not a soft market. That is a recovering one.

DFW continues to lead. The Metroplex has absorbed over 120 corporate relocations in five years and added an estimated 40,000 to 50,000 jobs in Dallas alone in the past year. Collin and Denton counties remain active for production builders. Ellis County is emerging as a lower land cost alternative for builders pushing south. National builders targeting infill and suburban submarkets are competing for sites with clear infrastructure and entitlement paths.

Houston is the volume leader. January 2026 residential construction value in the Houston metro approached $660 million, with Harris County anchoring activity across both infill and suburban submarkets. With an average new home construction value exceeding $383,000, the Dallas area continues to demonstrate strength in higher price-point segments — signaling that builders are not abandoning quality for volume.

Austin is the outlier. Starts are down roughly 15 percent from peak, and the market is absorbing oversupply from the pandemic-era construction surge. But Austin is structurally constrained — water access limits, entitlement complexity, and a compressed geography mean that well-located, entitled land with utility access rebounds quickly once demand stabilizes. Williamson County continues to attract sustained development interest due to land availability and infrastructure expansion relative to central Austin.

San Antonio is stable but cautious. Builders there operate with thinner lot pipelines and more self-development, which compresses the window for landowners presenting raw or partially entitled sites.

What Builders Are Actually Underwriting in 2026

Understanding builder demand in 2026 requires understanding builder discipline. These are not 2021 buyers. They are not paying for optionality. They are paying for execution certainty.

The variables that determine whether a site moves to contract are narrow and specific:

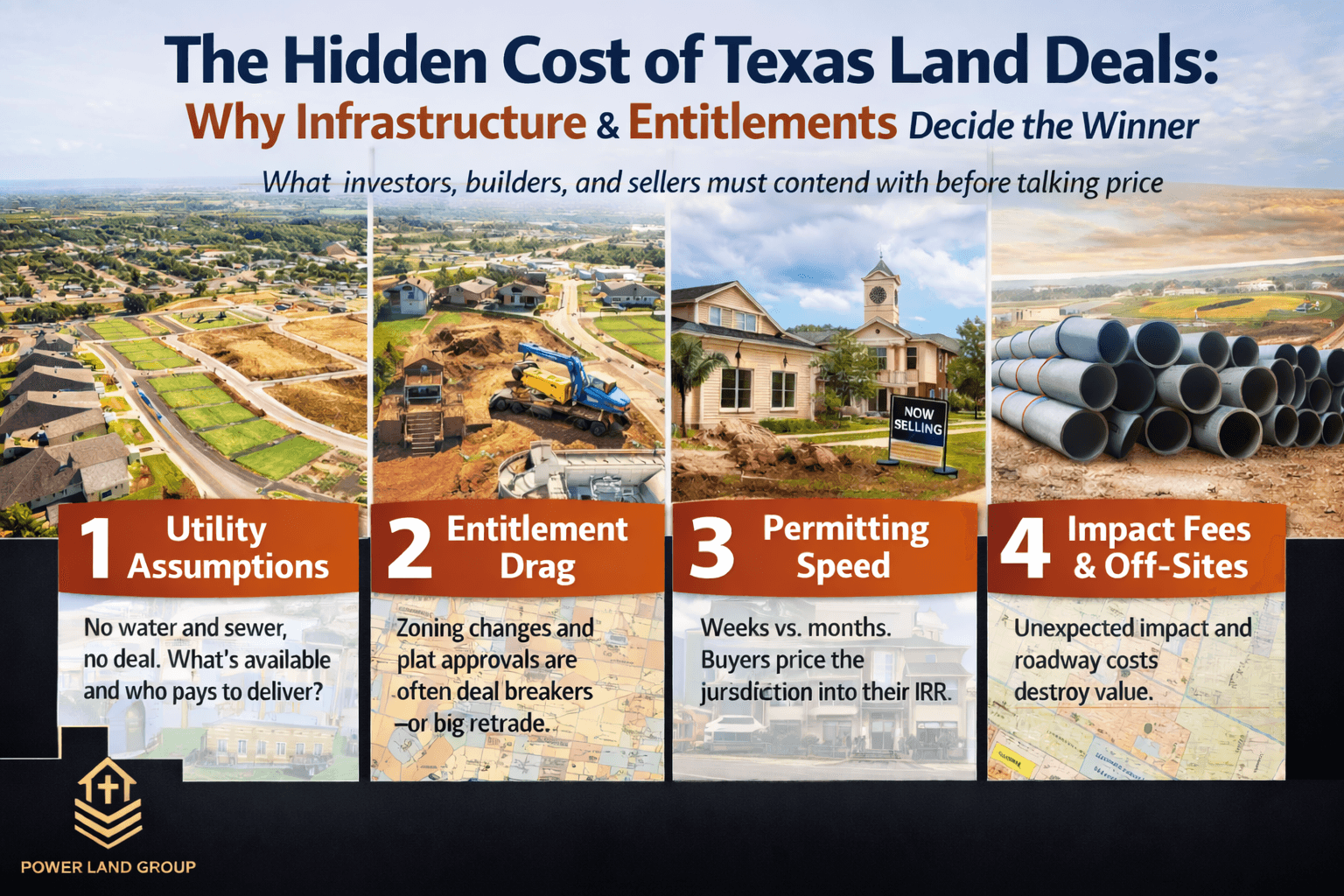

- Utility availability and capacity. North Texas Municipal Water District alone is investing an estimated $1.7 billion in 2026 capital improvements to keep pace with regional growth. Wholesale water rates are climbing — up 7.5 percent for 2026. Builders are stress-testing utility cost per lot before they discuss acquisition price. A site without a committed utility solution is a site without a buyer.

- Entitlement status and timeline. City-level permitting bottlenecks are delaying approvals in multiple suburban markets across DFW. Cities like Princeton have temporarily paused new development to address infrastructure capacity. Builders are not budgeting 18-to-24 month entitlement timelines into their return models without a significant discount at acquisition. Clear zoning and approved plats are being priced at a premium.

- Lot yield and product fit. Builders have adjusted across the board — smaller lots, simplified floor plans, attainable price points. A site that pencils for 5,000 square foot lots but not 7,500 square foot lots is a different deal. Landowners who have not modeled yield scenarios based on current builder product types are starting the conversation behind.

- Infrastructure cost exposure. Road improvements, water and wastewater extensions, and drainage infrastructure can represent millions per project. Builders are allocating those costs against land price at acquisition. A site priced without accounting for off-site infrastructure requirements will not close at ask.

- Execution timeline. Builders focused on moving standing inventory are not acquiring sites with multi-year execution timelines unless the basis reflects that risk. Time is being priced into every deal.

What Institutional Capital Is Watching

Private capital allocation to real estate is shifting in 2026. Institutional capital allocations to real assets continue to grow, particularly as investors seek inflation hedges and stable income. Family offices and private equity managers are actively evaluating Texas land — but they are doing so through the same underwriting lens as builders: utilities, entitlements, timeline, and realistic exit pricing.

Texas land has appreciated 7 to 9 percent annually since 2020, outperforming the national average. Development-grade land in the Austin-San Antonio corridor is priced at $100,000 to $500,000 per acre within 30 miles of downtown Austin. Northeast Texas land is holding at approximately $9,313 per acre despite lower transaction volume. The Austin-Waco-Hill Country region hit a record $7,704 per acre, with sales volume up 5.7 percent year over year.

But statewide, the forecast is measured. The Texas Real Estate Research Center projects nominal price per acre rising approximately 2 percent over the next four quarters. Total acres sold are expected to rise slowly in the second half of 2026. This is not a distress market, but it is not a speculation market either. Well-located properties with water access and entitlement clarity sell quickly. Everything else sits.

The Positioning Gap — And Where Landowners Are Losing Value

The most common mistake landowners make in a disciplined market is pricing their land based on comparable sales from 2022 or early 2023. Those comps reflect a different underwriting environment — lower interest rates, aggressive builder expansion, and institutional capital chasing yield at lower thresholds.

Today's buyer is running a different model. Mortgage rates are expected to remain above 6 percent through much of 2026. Builder margin pressure is real. Incentives to sell homes are compressing returns at the front end. Every dollar of acquisition cost above supportable land value flows directly into deal erosion.

Landowners who have not had a builder-lens evaluation of their site — not a broker opinion of value, but an actual underwriting of lots, utilities, entitlements, and timeline — are almost certainly either overpriced or underpositioned. Both outcomes cost money.

What Moves a Deal in This Market

Three things move land deals in Q1 2026:

- Transparent documentation. Utility letters, plat status, survey, flood plain determination, and title history presented upfront. Buyers are not conducting discovery on ambiguous sites.

- Pricing tied to builder economics. Land value is a function of finished lot value minus builder development cost minus builder margin. That math has to work. Sellers who start with a price and work backward from it rarely close in this market.

- Access to the right buyer. National and regional builders acquiring in Texas are running disciplined land programs with defined product types and geographic targets. Family offices and private equity platforms have specific size and basis thresholds. Off-market positioning to the right counterparty — before a site is widely shopped — consistently produces better outcomes than open-market processes for land.

The Window Is Open — But Buyers Are Selective

Texas fundamentals remain intact. Population growth, corporate relocation, and job formation continue to drive housing demand across DFW, Houston, San Antonio, and the Austin suburbs. Single-family permits are climbing. Infrastructure investment is accelerating. Institutional capital is looking for places to deploy.

But the market is selecting for prepared sellers. A landowner with clear entitlements, utility commitments, and a realistic price based on builder economics will transact. A landowner with a good location but an incomplete site package will wait — sometimes for years.

The difference between those two outcomes is often not the land. It is the preparation and positioning strategy.

If you want a confidential Land Value Opinion or want to discuss positioning your property for institutional buyers, PLG evaluates land the way builders do — utilities, entitlements, execution timeline, and realistic pricing before we ever discuss terms. Submit your property details at powerlandgroup.com.